A recent 60 Minutes segment on a U.S. shipyard spotlighted the renewed attention on America’s shipbuilding capacity and the strategic importance of strengthening industrial and maritime power at home — a priority the Trump Administration has elevated. But by focusing narrowly on a single shipyard and only a small slice of the 45,000-vessel U.S.-flag fleet, alongside commentary from a CATO activist, the piece risked presenting that snapshot as the full picture of America’s 650,000-strong maritime workforce. Below are five key areas where the record deserves correcting.

MYTH #1: The U.S. barely builds any ships.

FACT: The U.S. builds hundreds of vessels every year. WorkBoat’s annual construction surveys, the most expansive in the industry, documented 690 vessels under order, construction, or delivery in 2023, 925 in 2024, and 750 in 2025 — and all three surveys note these numbers could undercount the domestic shipyard industrial base due to commercial non-disclosure agreements. This spans Navy warships, Coast Guard cutters, ferries, research vessels, tugs, offshore wind support ships, and more.

MYTH #2: The Jones Act weakens American shipbuilding.

FACT: The Jones Act is what makes American shipbuilding possible. It guarantees a domestic market for U.S.-built vessels, directly sustaining nearly 650,000 jobs, $41 billion in annual wages, and over $154 billion in total economic output. Every container ship, tanker, articulated tug barge, towboat, ferry, pilot boat, and barge exists because of the Jones Act demand signal. As of 2023, the Bureau of Transportation Statistics puts the total number of U.S.-flagged vessels, largely qualified under the Jones Act, at over 45,000.

MYTH #3: U.S. ships cost more because American yards are inefficient.

FACT: The cost difference largely reflects that U.S. yards pay American wages, meet American safety and environmental standards, and comply with U.S. tax law — obligations foreign competitors don’t share in their home markets. MARAD found U.S. shipbuilding jobs pay nearly 50% above the national average wage. That premium reflects quality, not waste. Over the last ten years, South Korea has subsidized its shipyards with $40–50 billion in state-backed loans and guarantees, Japan has invested $10–$12 billion in subsidies for shipbuilding and repair, while China’s subsidies number $100– $130 billion. Meanwhile, the United States has invested only a few hundred million taxpayer dollars in workforce development programs and small shipyard grants over the same period.

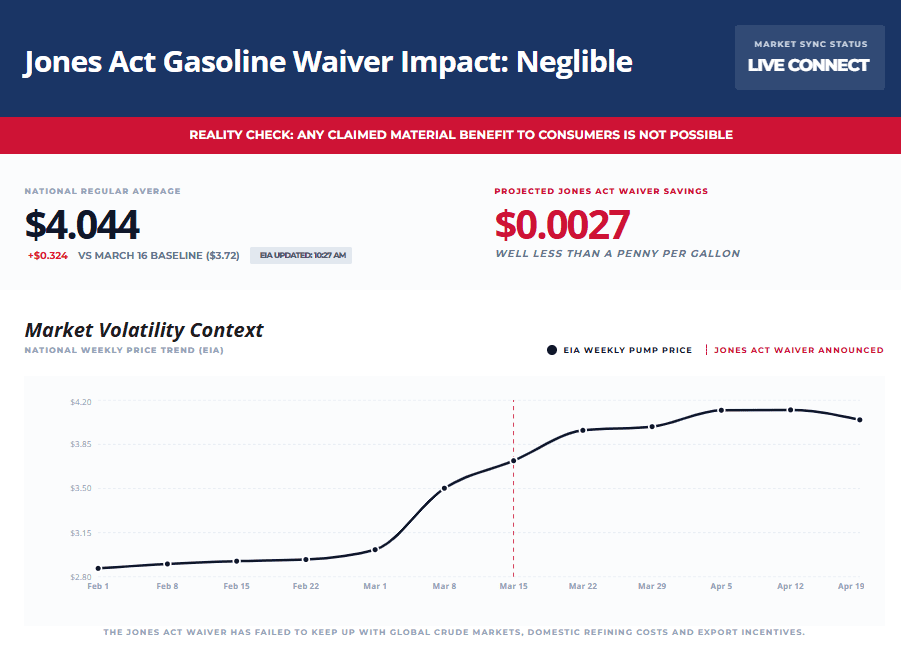

MYTH #4: The Jones Act leaves Americans without access to domestic energy.

FACT: The most efficient way to transport natural gas is by pipeline, which is why over 95% of gas is transported by pipeline. Natural gas, when put into a liquified state, trades at a world price because it is no longer confined to pipelines. American shipyards are ready to build LNG ships should the domestic market demand it. U.S. Shipyards build LNG vessels used for transport and to fuel LNG-powered vessels. A long-term supply contract is all that is needed to build a Jones Act-compliant large LNG ship.

MYTH #5: America has no shipbuilding expertise left.

FACT: U.S. yards currently build highly specialized vessels for the military, domestic and deep sea markets – aircraft carriers, nuclear submarines, missile destroyers, oceanographic research vessels, dredges, offshore supply vessels, self-unloading bulkers for the Great Lakes, tankers, container vessels and cable-laying vessels. Austal USA, Ingalls Shipbuilding, Fincantieri Marinette Marine, Eastern Shipbuilding, and dozens of other yards represent a deep, active industrial base — not a relic. These shipyards are capable of building both vessels of over 1,000 gross tons, the standard for oceangoing ships, and smaller purpose-built craft. The claim that there are only “two major shipyards” in the United States does not hold water.

Contact the American Maritime Partnership if you have questions about the size and strength of the U.S. Jones Act:

Comments are closed.